Cotton freight insurance safeguards your cotton shipments from theft, damage, and other transit risks. With cargo theft up by 1,500% since 2021 and average losses per incident reaching $200,000, this insurance ensures financial security beyond the limited liability of carriers. Coverage options range from all-risks policies, which protect against most transit issues, to basic Free of Particular Average (FPA) coverage for catastrophic events. Premiums typically cost 0.3%–1% of the shipment's insured value, making it a practical choice for high-value cotton goods. Proper documentation and timely claims filing are crucial for reimbursement. This insurance is a must for businesses relying on cotton transport to maintain smooth operations and reduce financial exposure.

Marine Insurance Explained - Understand the Cargo Insurance You're Getting

sbb-itb-0e617ca

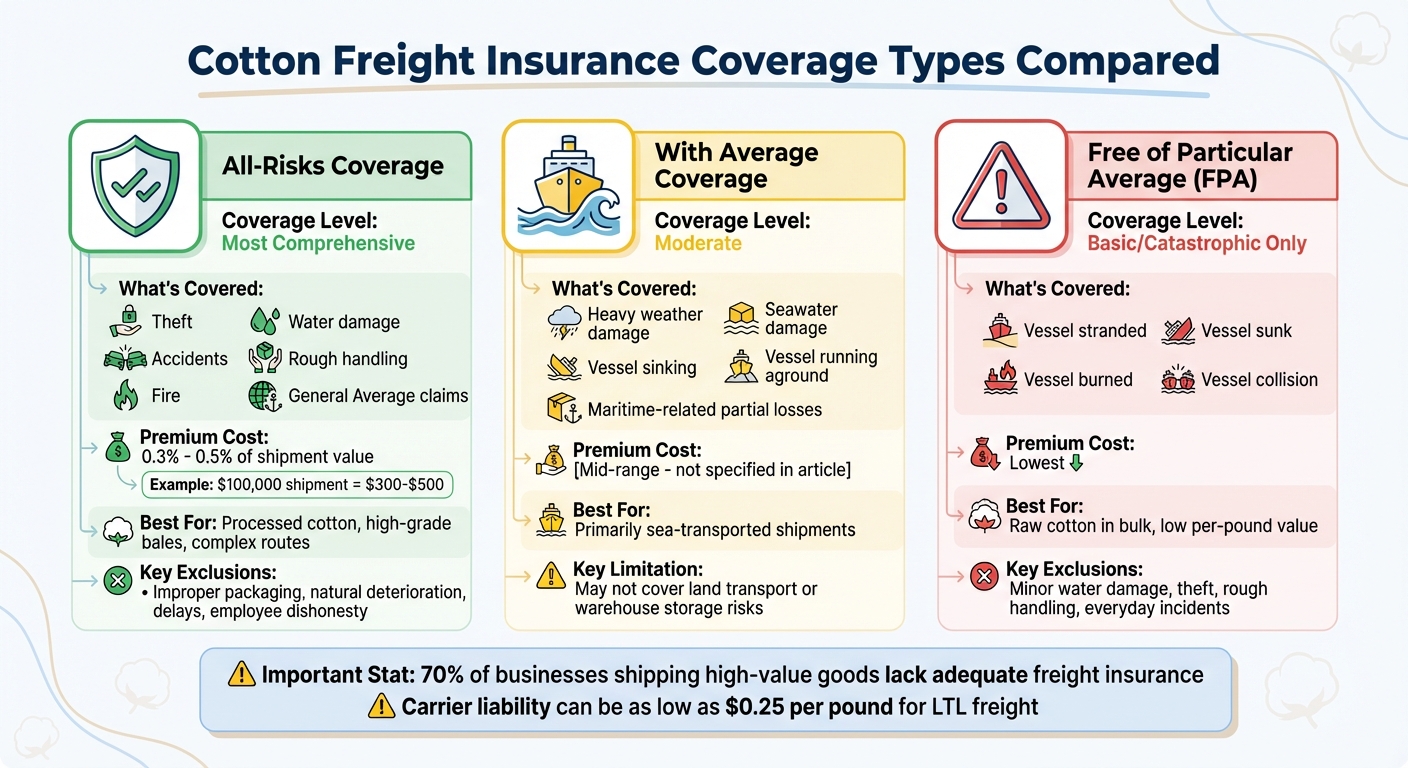

Types of Coverage for Cotton Freight Insurance

Cotton Freight Insurance Coverage Types Comparison Chart

Transporting cotton comes with its fair share of risks, making it essential to choose the right insurance coverage. Cotton freight insurance typically offers three main types of coverage, each designed to address different levels of risk. Let’s break them down to help you understand their scope and limitations.

All-Risks Coverage

This is the most extensive protection you can get for cotton shipments. All-risks coverage shields your goods from nearly every external cause of loss or damage during transit, whether it’s theft, accidents, fire, water damage, or rough handling. It’s especially useful for addressing the gaps in standard carrier liability, which often falls short when it comes to compensating for damages.

One standout feature of this coverage is its protection against General Average. Under maritime law, if sacrifices are made to save a vessel - like jettisoning cargo - all parties involved must share the costs. Without all-risks coverage, you’d be responsible for covering your share of these expenses upfront, and your cargo could even be detained until payment is made. With this policy, your insurer takes care of these claims, saving you from financial strain and delays.

"All Risk is a term which describes a broad form of coverage. It does not cover every scenario. Each policy comes with terms, conditions and exclusions." - Crowley

The cost for all-risks coverage usually falls between 0.3% and 0.5% of your shipment’s commercial invoice value. For instance, insuring a $100,000 shipment would cost $300 to $500. This makes it a smart choice for processed cotton or high-grade bales traveling through complex routes, where the chances of damage increase with multiple transfers.

However, it’s important to note that even all-risks policies have exclusions. Losses from improper packaging, natural deterioration (inherent vice), delays, or employee dishonesty are generally not covered. Alarmingly, about 70% of businesses shipping high-value goods lack adequate freight insurance, often relying on carrier liability, which can be as low as $0.25 per pound for certain shipments like less-than-truckload (LTL) freight.

With Average Coverage

If all-risks coverage feels too expansive or costly, With Average Coverage offers a middle ground. This type of insurance focuses on maritime risks, covering partial losses caused by sea-related perils like heavy weather or seawater damage, as well as major disasters such as a vessel sinking or running aground. It’s an excellent option for shipments primarily transported by sea, though it might not cover risks encountered during land transport or storage at warehouses.

Free of Particular Average Coverage

Free of Particular Average (FPA) Coverage provides the most basic level of protection. It only covers catastrophic events such as a vessel being stranded, sunk, burned, or involved in a collision. Everyday incidents like minor water damage, theft, or rough handling are excluded unless they stem directly from one of these major events.

This coverage is better suited for raw cotton transported in bulk, where the per-pound value is relatively low, and partial losses are less financially impactful. However, combining FPA with minimal carrier coverage can leave significant gaps, especially for higher-value shipments that require more comprehensive protection.

Common Risks During Cotton Transportation

Transporting cotton from its origin to its destination involves a range of challenges, making comprehensive freight insurance a necessity to protect against potential losses. Here’s a closer look at the risks cotton shipments face along the supply chain.

Physical damage from accidents is a major concern. Incidents like truck collisions, vehicle overturns, or impacts during terminal handling can crush cotton bales or tear their packaging, leading to partial or complete loss. These risks are especially prevalent on long-haul routes with multiple transfers. Beyond accidents, theft adds another layer of vulnerability to shipments.

Theft continues to be a significant issue in the shipping industry. In fact, theft during transit accounts for 71% of all reported shipping incidents, with the average loss per theft estimated at $200,000. Thieves often target entire shipments, but pilferage - stealing smaller portions of cargo - is also common, leaving shipments exposed at every stage of transportation.

Environmental and weather-related damage is another critical risk for cotton, which is highly sensitive to moisture. Exposure to rain, floods, hurricanes, or high humidity during loading or transit can lead to mold, fiber deterioration, and discoloration. Cotton’s flammability further increases its risk of fire or explosions, whether during transportation or at transload points. Additionally, improper storage, rough handling, or equipment failures can cause significant damage to the bales.

When dealing with international shipments, maritime-specific risks come into play. Severe weather can lead to cargo being lost overboard or even jettisoned as part of General Average sacrifices to save a distressed vessel. Other natural risks include shrinkage, insect or pest damage, and inherent vice - where the organic material naturally deteriorates - potentially compromising the shipment’s quality before it even arrives at its destination.

| Risk Category | Specific Examples | Potential Impact |

|---|---|---|

| Transit Accidents | Collisions, overturns, terminal impacts | Severe crushing or total loss |

| Crime | Theft, pilferage, cargo fraud | Financial loss and supply chain delays |

| Environmental | Moisture, floods, storms, fire | Rot, mold, or fiber destruction |

| Operational | Rough handling, improper loading | Packaging failure or torn bales |

| Biological | Insect damage, inherent vice | Quality degradation or customs rejection |

How to File a Cotton Freight Insurance Claim

When dealing with damaged or missing cotton shipments, acting quickly and documenting everything thoroughly is key to a successful claim. If you notice visible damage, make sure it's recorded on the Proof of Delivery (POD) before the driver leaves - this step is crucial to avoid claim rejection. For concealed damage discovered after unboxing, notify the carrier within 5 business days. In the U.S., you have 9 months from the delivery date to file a written claim for domestic trucking shipments.

To build a strong claim, gather all the necessary documents to verify the loss and its value. These typically include the Bill of Lading (BOL), the commercial invoice with updated HS codes, a packing list, and weight tickets (especially important for bulk cotton shipments to prove shortages). Take clear, timestamped photos and videos of the damaged cotton from multiple angles, including during the unboxing process. Keep all original packaging intact and avoid moving the damaged cotton, as carriers may require a post-claim inspection. Poor or incomplete documentation is one of the main reasons - about 70% - for cargo insurance claim denials.

Carriers are required to acknowledge your claim within 30 days and settle it within 120 days. However, make sure all freight charges are fully paid before filing your claim, as many carriers won’t process claims until the original shipping invoice is cleared. If your claim is denied, contact your insurance broker immediately to understand the reason and have them advocate for you.

"Negotiate, mediate, arbitrate and only then litigate. Litigation against an insurance carrier should be the arrow of last resort in the quiver." - Lance Ewing, EVP of Risk Management at Cotton

If your claim is denied, address the specific reason with focused evidence, such as policy language, survey reports, or corrected documents, rather than making broad arguments. Once you’re familiar with the claims process, it’s easier to assess which insurance policy best fits your needs.

Selecting the Right Insurance Policy for Cotton Gin Operators

Assessing Your Coverage Requirements

Standard All-Risk freight policies often exclude cotton from their coverage. This means cotton gin operators typically need specialized agribusiness policies or specific endorsements tailored to their commodity. Cotton comes with unique risks, such as spontaneous combustion caused by microbial self-heating in lint and cottonseed, which can be particularly hazardous for ginning operations.

"Spontaneous combustion... can occur when the natural organic substances within the cotton catch fire and ignite on their own, without apparent cause from outside forces... Some consider spontaneous combustion as the greatest risk for cotton-producing and ginning." - Arnold Insurance

To ensure full protection, cotton should be insured from the moment it’s picked in the field, through the ginning process (via a Gin Stock Floater), and during its final transit. You may also want to consider additional coverage options such as machinery breakdown insurance for ginning equipment, electronic equipment insurance for power surges, and Loss of Profit coverage. This last option can be invaluable if equipment failures or transit losses disrupt your ability to meet production targets.

Because standard policies often exclude these critical risks, specialized endorsements are essential. Research indicates that up to 30% of transit-related losses are unavoidable, making tailored coverage even more important.

Comparing Policy Costs and Coverage Terms

When evaluating policies, ensure that the "insured value" accurately reflects your actual commercial interest. This should include seasonal price fluctuations and freight charges, not just the carrier's limited liability. Carefully review exclusions for issues like "inherent vice" (natural deterioration), poor packaging, or delays that don’t involve physical damage.

Deductibles play a significant role in determining both your premium and your financial responsibility in the event of a claim. Typical deductible structures include:

- $0 for insured values up to $10,000

- $500 for $10,000.01–$25,000

- $1,000 for $25,000.01–$100,000

- 2% for values over $100,000

For truckload shipments, the deductible is often $1,000 for values up to $100,000, with 2% applied beyond that threshold. Selecting a deductible that balances lower premiums with manageable out-of-pocket costs is key.

You can also reduce insurance costs by demonstrating improved risk management practices. For example, better packaging standards, moisture control, and traceability measures (like pallet IDs and seal records) can lower premiums during policy renewal. High-quality photos of cotton loads and packaging before shipping can streamline claims and may even help secure reduced rates.

By understanding these factors and leveraging industry connections, operators can fine-tune their insurance strategies to better manage risks.

Using cottongins.org for Industry Resources

In addition to policy considerations, tapping into industry resources can strengthen your overall risk management approach. The cottongins.org directory connects cotton professionals across the United States, providing a platform to share insights and access local resources. Gin operators can use the directory to exchange experiences about freight insurance and coverage options with peers in their region.

The platform also offers sponsorship opportunities, enabling insurance providers and service companies to connect directly with gin operators. This creates a valuable network for both learning and collaboration, helping operators make more informed decisions about their insurance needs.

Conclusion

Cotton freight insurance offers critical financial protection that goes beyond the limits of standard carrier liability. As highlighted earlier, the gap between the actual value of cargo and available compensation can lead to severe financial losses. By transferring this risk to an insurer, you ensure stability and predictable outcomes, even in the face of theft, weather-related damage, or mishandling during transit.

The risks in today's shipping environment are undeniable. Cargo theft alone has skyrocketed by 1,500% since early 2021, with an average loss of $200,000 per incident. For cotton gin operators, who face unique challenges like spontaneous combustion risks and multi-stage handling, having comprehensive insurance isn't just a smart move - it's essential for protecting the business.

"Freight insurance should be viewed not as an optional expense but as an essential risk management tool - particularly for high-value, fragile, or time-sensitive shipments." - FreighterGator

Freight insurance also helps maintain strong customer relationships by enabling quick replacements and keeping operations running smoothly. At a cost of just 0.3% to 1% of the cargo's value, it offers robust protection without straining your budget.

To stay ahead of evolving risks, review your policy annually. Make sure it aligns with current shipping patterns, cargo values, and potential threats. Keep thorough documentation, including pre-shipment photos and delivery receipts, to make claims easier if needed. With the right coverage in place, you can focus on growing your business instead of worrying about potential setbacks during transit.

FAQs

Does cotton freight insurance cover theft at a warehouse or only in transit?

Cotton freight insurance generally provides coverage for theft that occurs during transit. In some cases, it might also extend to theft at warehouses, but this depends on the specific terms outlined in your policy. It's important to review your policy details carefully to see if protection for storage facilities is included.

How do I calculate the right insured value for a cotton shipment?

To figure out the insured value, start by adding the commercial invoice value of the cotton to the freight cost. Then, tack on an additional 10% to cover potential expenses like customs or handling fees. Be sure to review your policy's valuation clause, as the exact requirements can differ. Avoid underestimating the value - doing so could result in underinsurance. Make sure the total accurately represents the shipment's full cost to ensure proper coverage.

What exclusions should cotton shippers watch for in all-risk policies?

Cotton shippers need to pay close attention to the exclusions commonly found in all-risk insurance policies. These exclusions often include intentional acts, illegal activities, maintenance-related issues, and risks already covered under other policies. Failing to account for these could result in denied claims for certain incidents. It's crucial to thoroughly review the policy details to avoid surprises.