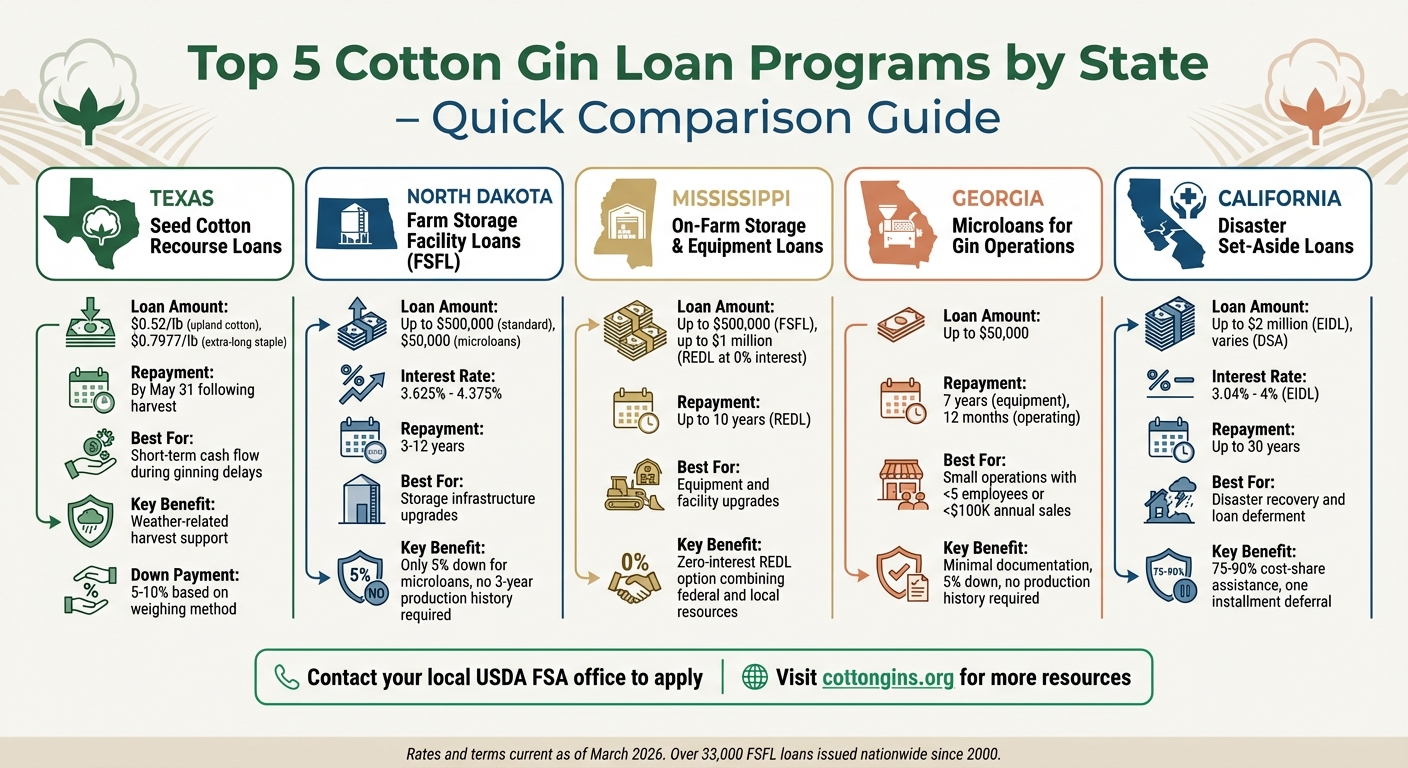

Running a cotton gin business can get expensive, especially with the need for specialized equipment and storage. Luckily, several loan programs are available to help cotton gin operators manage costs and improve operations. Here’s a quick look at five state-specific programs tailored to support cotton producers:

- Texas Seed Cotton Recourse Loans: Offers short-term financing at $0.52/lb for upland cotton and $0.7977/lb for extra-long staple cotton, helping producers during delayed ginning periods.

- North Dakota Farm Storage Facility Loans (FSFL): Provides up to $500,000 for storage upgrades, with microloans available for smaller projects requiring just a 5% down payment.

- Mississippi On-Farm Storage and Equipment Loans: Combines federal FSFL funds with local resources, offering up to $1 million through zero-interest loans for equipment and facility upgrades.

- Georgia Microloans for Gin Operations: Targets smaller businesses with loans up to $50,000, requiring minimal down payments and flexible terms.

- California Disaster Set-Aside Loans: Supports cotton gin operators affected by natural disasters by deferring loan repayments and offering additional disaster relief funding.

Each program addresses unique challenges faced by cotton gin businesses in its respective state, whether it’s managing cash flow, upgrading infrastructure, or recovering from natural disasters.

Quick Comparison

| Program | Loan Amount | Key Features | Eligibility |

|---|---|---|---|

| Texas Seed Cotton Loans | $0.52/lb upland, $0.7977/lb ELS | Short-term financing for delayed ginning | Cotton stored in modules, not yet ginned, and insured against fire |

| North Dakota FSFL | Up to $500,000 ($50,000 for microloans) | Low-interest loans for storage upgrades; 5% down for microloans | Landowners, tenants, or sharecroppers producing eligible commodities |

| Mississippi Equipment Loans | Up to $1 million (zero-interest) | Combines FSFL funding with local resources for equipment and facility upgrades | Proof of storage or equipment need; compliance with federal and state requirements |

| Georgia Microloans | Up to $50,000 | Flexible terms, minimal down payment, and no 3-year production history requirement | Small businesses with fewer than 5 employees or annual sales under $100,000 |

| California Disaster Loans | Varies | Defers loan repayments and offers disaster recovery funding | Existing FSA direct loan borrowers affected by federally declared disasters |

Reach out to your local USDA FSA office to learn more and find the program that fits your needs.

Cotton Gin Loan Programs Comparison by State

Navigate Farm Loans Easily with FSA's New Online Feature | Tuesday Seeds with Joshua Coleman

sbb-itb-0e617ca

1. Texas Seed Cotton Recourse Loans

Texas cotton producers dealing with delayed ginning have access to specialized recourse loans that provide temporary financing while their cotton remains stored in module form. These loans are crafted to address the unique challenges Texas farmers face, offering much-needed cash flow support when weather conditions or heavy harvests slow the ginning process.

Loan Amount and Terms

The program provides loans at rates of $0.52 per pound for upland cotton and $0.7977 per pound for extra-long staple cotton. The loan quantity is calculated by multiplying the weight of the seed cotton by a lint turnout factor - 32% for machine-picked cotton and 22% for machine-stripped cotton. Producers can borrow up to 95% of the estimated lint value if the seed cotton is weighed, or 90% if it is measured.

Loans must be repaid by May 31 of the year following the harvest. Repayment can be made in cash or through proceeds from a ginned cotton nonrecourse marketing assistance loan. A non-refundable service fee, determined by the Commodity Credit Corporation, is also required.

Eligibility Requirements

Eligible applicants include individuals, partnerships, corporations, estates, and trusts involved in cotton production as landowners, landlords, tenants, or sharecroppers. The cotton must be harvested but not yet ginned, stored in module form either on-farm or off-farm, but not in public warehouses. Producers must retain beneficial interest (title, possession, and control) until the loan is repaid and must file a timely acreage certification for all cropland on the farm. Additionally, the seed cotton must be insured at its full loan value against fire damage.

Once eligibility is confirmed, producers can move forward with a straightforward application process.

Application Process

To apply, producers must visit their local FSA county office by March 31 of the year following the harvest. FSA staff assist with completing the necessary note and security agreements and inspect the seed cotton modules to determine the loan quantity. After verifying the cotton's condition and completing the paperwork, the loan proceeds are disbursed, minus any service charges.

State-specific Benefits

Gary Six, FSA State Executive Director in Texas, highlighted the program’s importance, especially during challenging harvest conditions:

"While the rain we received this fall in Texas was a welcome relief for our drought-stricken areas, it also slowed down harvest. Here in Texas and elsewhere across the country, we're making sure producers know about seed cotton recourse loans, which can help meet our producers' financial needs."

This program is tailored to address the unpredictable weather and harvest challenges Texas cotton producers face. By providing financial flexibility, it supports farmers during critical growing seasons and complements broader USDA initiatives aimed at sustaining cotton gin businesses and the agricultural economy.

2. North Dakota Farm Storage Facility Loans

Farmers and agricultural producers in North Dakota, including those involved in cotton gin operations, can benefit from the Farm Storage Facility Loan (FSFL) program. This program provides low-interest loans to help build or upgrade essential infrastructure like grain bins, storage facilities, and handling equipment. By supporting these improvements, the FSFL program plays a key role in helping producers manage their harvests efficiently.

Loan Amount and Terms

The FSFL program offers financing up to $500,000 for storage facilities and $100,000 for trucks. Loan repayment terms range from 3 to 12 years, with interest rates between 3.625% and 4.375% as of March 2026. On average, loans awarded in fiscal year 2026 are expected to be around $125,000.

For smaller projects, a microloan option is available, offering up to $50,000 with just a 5% down payment and no requirement for three years of production history. Since the program began in May 2000, over 33,000 loans have been issued, adding an impressive 900 million bushels of storage capacity nationwide.

Eligibility Requirements

To qualify, applicants must be landowners, operators, tenants, leaseholders, or sharecroppers who produce eligible commodities. Other requirements include:

- A solid credit history and demonstrated repayment ability.

- No outstanding Federal debt.

- Proof of the need for additional storage capacity.

- Crop insurance for economically significant crops in the area.

- Compliance with USDA regulations on highly erodible land and wetlands, as well as local building and zoning codes.

Application Process

Applications must be submitted to the local FSA county office, along with a $100 non-refundable application fee. The approval process typically takes 2 to 6 weeks, and construction can only begin after receiving local FSA approval and completing the required environmental evaluation. Loans are secured through a promissory note, security agreement, and a UCC-1 filing.

State-specific Benefits

North Dakota producers also enjoy additional resources during challenging times, like natural disasters. For example, those affected by disasters between December 1, 2021, and August 1, 2022, could access the Emergency Grain Storage Facility Assistance Program (EGSFP). This program provided 75% to 90% cost-share assistance for new or renovated storage facilities, with socially disadvantaged, beginning, or veteran farmers qualifying for the higher 90% rate.

Additionally, North Dakota's Ag PACE program offers interest rate reductions for farmers investing in equipment or facilities aimed at nontraditional agricultural activities.

3. Mississippi On-Farm Storage and Equipment Loans

Mississippi has developed loan programs that blend federal initiatives with local resources, creating financial opportunities tailored to the state's agricultural needs. For example, cotton gin operators in Mississippi can take advantage of the Farm Storage Facility Loan (FSFL) program, which provides funding for infrastructure. This program offers up to $500,000 for storage facilities and $100,000 for handling trucks. The loan terms align with national FSFL standards, ensuring competitive options for local producers.

Loan Amount and Terms

Mississippi producers can access the FSFL microloan option, which offers up to $50,000 with just a 5% down payment and no requirement for a three-year production history. Beyond FSFL, the Rural Economic Development Loan (REDL) program is another valuable resource. This program provides zero-interest loans of up to $1 million for equipment and facility upgrades, with a repayment term of up to 10 years.

Eligibility Requirements

To qualify, applicants must be landowners, operators, tenants, leaseholders, or sharecroppers involved in producing upland or extra-long staple cotton. Key eligibility criteria include:

- A satisfactory credit history

- No delinquent federal debt

- Proof of need for additional storage capacity

Additionally, cotton producers must submit Form CCC-633EZ Page 1 to their local FSA office before losing beneficial interest in their crop.

Application Process

The process starts with submitting Form CCC-0185 at the local FSA county office. It’s crucial to complete the required environmental review before starting any site work, as skipping this step could result in loan denial. Applicants must also provide all necessary permits and documentation. Mississippi producers can use customer kiosks at county offices for signing documents and accessing the Loan Assistance Tool.

State-Specific Benefits

Mississippi farmers also benefit from programs like the Mississippi Land Bank, which offers financing options tailored to production cycles for tractors, harvest equipment, and irrigation systems. The Land Bank has returned nearly $70 million to customers through its cash patronage program.

Demetrice Evans, Deputy State Executive Director in Mississippi, highlights the importance of these programs:

"Under current market conditions, Loan Deficiency Payments can provide cash flow and help cotton producers stabilize farm income and manage risk".

4. Georgia Microloans for Gin Operations

In Georgia, gin operators have access to microloans designed specifically for small-scale and nontraditional agricultural businesses. The USDA Farm Service Agency (FSA) Microloan program, supported by the Georgia Soil and Water Conservation Commission, offers flexible credit solutions to meet the unique needs of new and nontraditional farm operations. These programs are especially helpful for gin businesses that may not qualify for traditional financing. Below, we break down the program details, including terms, eligibility, application steps, and benefits specific to Georgia.

Loan Amount and Terms

The FSA Microloan program provides loans of up to $50,000 with flexible repayment options. Borrowers can repay loans over 7 years for equipment and general purchases or 12 months for operating loans. Interest rates are determined based on the Operating Loan rates in effect at the time of either approval or closing - whichever is lower. Additionally, the Rural Microentrepreneur Assistance Program (RMAP) offers fixed-rate loans, though these are limited to covering 75% of the total project cost.

Eligibility Requirements

Eligibility varies depending on the size and scope of the business:

- Small businesses with 5 or fewer employees and annual sales under $100,000 can apply through Community Development Financial Institutions.

- Larger cotton gin operations with up to 750 employees may qualify under the Georgia Loan Participation Program, though it primarily targets businesses with 500 or fewer employees.

Loan funds must be used for specific business purposes, such as purchasing machinery, equipment, inventory, working capital, or for facility construction and renovation. Some programs may require applicants to show proof of denial from a conventional lender and contribute at least a 10% equity stake in the project.

Application Process

To get started, applicants should contact the Georgia Development Authority Administrative Office in Monroe or their local branch for detailed requirements. A complete application typically includes:

- A Farm Balance Sheet and Income Statement to demonstrate financial stability.

- Supporting documents such as a Loan Checklist, Credit Inquiry Letter, Service Provider Reimbursement form, and Borrowers Release Authorization.

Because the preparation process can take several months, it’s best to reach out to your local USDA Service Center or the Georgia State Office of Rural Development early in the planning stages.

State-Specific Benefits

Georgia offers additional support for gin operators through programs like AgGeorgia Farm Credit, which assists "Young, Beginning, and Small" (YBS) farmers with annual revenues under $350,000. For those who don’t meet traditional financing criteria, an FSA guarantee on an AgGeorgia loan may be an option. The AGAware® Program also provides financial literacy and business workshops to help young and small-scale farmers build long-term success. These initiatives highlight Georgia's efforts to address the unique financial challenges faced by cotton gin businesses of varying sizes and structures.

5. California Disaster Set-Aside Loans

California cotton gin operators affected by natural disasters have access to relief programs designed to ease financial strain. One such option is the Disaster Set-Aside (DSA) program, managed by the USDA Farm Service Agency (FSA). This program allows borrowers with existing FSA direct loans to defer one annual installment to the end of their loan term, providing flexibility across various FSA loan types. According to the USDA Farm Service Agency:

"This set-aside installment helps producers regain their financial footing without facing immediate repayment pressure, enabling them to focus on recovery efforts".

Loan Amount and Terms

The DSA program focuses on deferring one installment per loan to the end of its term. For additional funding, the SBA Economic Injury Disaster Loans (EIDL) can provide up to $2,000,000 with interest rates ranging from 3.04% to 4%, offering repayment terms as long as 30 years. Meanwhile, California's Nor-Cal FDC Disaster Relief Loan Guarantee program can guarantee up to 90% of a loan, with a maximum guarantee of $2.5 million and terms of up to 7 years. These options work together to provide financial relief for cotton gin operators, helping them recover from disaster-related losses.

Eligibility Requirements

To qualify for the DSA program, applicants must already have an FSA direct loan and must have been current - or no more than 90 days overdue - on their payments before the disaster struck. Additionally, they must demonstrate that the disaster, such as wildfires, floods, or excessive heat, directly impacted their ability to meet scheduled payments. The operation must also be located in a federally declared disaster area or a neighboring county. This includes key cotton-producing regions like Fresno, Kern, Kings, and Madera.

For SBA disaster loans, cotton gins often qualify as "nonfarm" processing businesses or agricultural cooperatives, even though businesses primarily engaged in farming or ranching are typically ineligible.

Application Process

To apply for the DSA program, operators need to submit a written request within eight months of the disaster designation. Required documents include tax returns, proof of ownership or lease agreements, and evidence of property damage. For SBA disaster loans, Tanya N. Garfield, Director of SBA's Disaster Field Operations Center-West, explains:

"SBA eligibility covers both the economic impacts on businesses dependent on farmers and ranchers that have suffered agricultural production losses caused by the disaster and businesses directly impacted by the disaster".

State-Specific Benefits

California cotton gin operators benefit from a range of state and federal disaster relief programs. The American Relief Act of 2025 allocated disaster recovery funds to the USDA, with the Supplemental Disaster Relief Program (SDRP) addressing eligible crop losses from 2023 and 2024. Additionally, California's IBank Small Business Disaster Relief Loan Guarantee Program offers guarantees of up to 95% for loans, with a maximum guarantee of $1 million. Together, these programs provide both immediate financial assistance and long-term recovery support, ensuring that cotton gin businesses in California have access to the resources they need to rebuild and thrive.

Program Comparison

When choosing a cotton gin loan program, it’s essential to weigh the features that align with your operation's needs. Below, you'll find a breakdown of loan options, highlighting maximum amounts, interest rates (as of March 2026), repayment terms, and unique state-specific benefits.

| Program | Max Loan Amount | Interest Rate | Repayment Period | Key Eligibility | State Advantage |

|---|---|---|---|---|---|

| Texas Seed Cotton Recourse Loans | $0.52/lb upland; $0.7977/lb ELS | $0.52/lb (upland); $0.7977/lb (ELS) | Short-term financing | Producers with harvested cotton in module form, not yet ginned | Helps manage cash flow during ginning delays caused by weather or increased acreage |

| North Dakota Farm Storage Facility Loans | Up to $500,000 (standard); $50,000 (microloans) | As detailed above | 3 to 12 years | Small/mid-sized farms; offers microloans without a 3-year production history requirement | Microloans require only a 5% down payment compared to 15% for standard loans |

| Mississippi On-Farm Storage and Equipment Loans | Up to $500,000 (FSFL); varies (B&I) | As detailed above | 3 to 12 years (FSFL) | Producers needing storage/handling equipment; B&I loans provide additional funding for rural businesses | B&I loans include an 80% guarantee (FY 2025) with a 3% initial fee and a 0.55% annual retention fee |

| Georgia Microloans for Gin Operations | Up to $50,000 | As detailed above | 3 to 12 years | Small operations; no 3-year production history required | Simplified documentation and a 5% down payment requirement |

Additionally, Business & Industry (B&I) Loan Guarantees in Mississippi and Texas stand out for larger operations. These loans offer an 80% guarantee for approvals in Fiscal Year 2025, which can be especially appealing to cooperatives and larger gin setups. However, they come with a 3% initial guarantee fee and a 0.55% annual retention fee on the outstanding principal. Cotton bales used as collateral must meet specific weight requirements - bales must weigh at least 325 pounds, and those over 600 pounds are capped at the 600-pound limit.

All programs require producers to maintain full control over their crops during the loan period. Compliance with Highly Erodible Land and Wetland Conservation provisions and Average Adjusted Gross Income (AGI) limitations is also mandatory.

Conclusion

Selecting the right loan program can make all the difference for your cotton gin operation, whether you're addressing immediate challenges or planning for long-term growth. Texas Seed Cotton Recourse Loans are ideal for short-term cash flow needs during harvest, while Farm Storage Facility Loans in North Dakota and Mississippi provide terms ranging from 3 to 12 years for infrastructure improvements. In Georgia, Microloans cater to smaller operations with just a 5% down payment and no need for a three-year production history requirement. For larger operations, the Business & Industry Loan Guarantees program offers an 80% guarantee for approvals in Fiscal Year 2025. Meanwhile, California’s disaster assistance programs provide cost-share support ranging from 75% to 90% for producers impacted by natural disasters.

These programs are tailored to address the diverse financial needs of cotton gin businesses, from managing short-term cash flow to funding large-scale infrastructure projects. By understanding the specific advantages each program offers, you can make informed decisions that align with your goals and operational priorities.

For more information on eligibility and application requirements, reach out to your local USDA FSA office. Programs like the FSFL, which has issued over 33,000 loans and expanded storage capacity by 900 million bushels since May 2000, demonstrate a strong track record of success. To explore cotton gin locations nationwide and access additional resources, visit cottongins.org. With the right preparation, you can confidently tackle financing challenges and choose the program that best supports your operation’s timeline, funding needs, and growth aspirations.

FAQs

Which loan program fits my cotton gin’s needs best?

The best loan program for your cotton gin will depend on several factors, including the size of your operation, your cash flow, and your specific financing needs. Here’s a quick breakdown of some options:

- USDA Loan Programs: These loans often come with long-term, low-interest rates, making them a great choice for those looking for more affordable financing options.

- Rural Energy for America Program (REAP): If energy efficiency or renewable energy projects are part of your plans, this program could be a good fit.

- Traditional Bank Loans or Private Financing: These options tend to work well for businesses with strong credit histories and established financial standing.

- State-Specific Programs: For smaller operations, localized programs like Missouri's Agribusiness Revolving Loan Fund can offer more tailored solutions designed to meet regional needs.

Each option has its own advantages, so it’s worth considering which aligns best with your goals and financial situation.

What documents do I need to apply at the USDA FSA office?

To apply for a loan through the USDA FSA office, you’ll generally need a few key documents. These include proof of ownership or control of the cotton, financial records that demonstrate your ability to repay the loan, and security documentation tied to the loan. Additionally, you must maintain beneficial interest in the cotton until the loan has been fully repaid. It’s a good idea to reach out to your local FSA office to confirm the exact requirements and make sure you’ve gathered all the necessary paperwork.

Can I combine FSFL, microloans, and disaster relief funding?

Yes, you can use FSFL (Farm Storage Facility Loans), microloans, and disaster relief funding together. These programs, offered by the USDA Farm Service Agency, are designed for different purposes, which means they can complement one another to address a range of needs. However, each program comes with its own set of eligibility criteria and application process. Make sure to review the details for each program thoroughly to confirm you meet the requirements for all of them.